Autocorrelation is the coefficient of linear correlation between two terms of a sequence of random variables.

Autocorrelation is also called serial correlation.

![]()

The following is formal definition.

Definition

Let

![]() be a sequence of random variables. The autocorrelation coefficient between two

terms of the sequence

be a sequence of random variables. The autocorrelation coefficient between two

terms of the sequence

![]() and

and

![]() is

is![[eq2]](/images/autocorrelation__4.png)

In other words, the autocorrelation coefficient is just the coefficient of linear correlation between two random variables belonging to the same sequence.

Note that the covariance

![]() is called autocovariance.

is called autocovariance.

Remember that a sequence of random variables is said to be covariance stationary (or weakly stationary) if and only if:

all the terms of the sequence have the same

mean:![]()

the covariance between any two terms of the sequence depends only on on how

far apart they are located from each other, and not on where they are located

in the

sequence:![]()

The second of these two properties implies that all the random variables in

the sequence have the same

variance:![]() because

because

![]() .

.

When a sequence is covariance stationary, the autocorrelation coefficient

between two terms of the sequence

![]() and

and

![]() depends only on

depends only on

![]() :

:![[eq8]](data:image/gif;base64,R0lGODlhAQABAIAAANvf7wAAACH5BAEAAAAALAAAAAABAAEAAAICRAEAOw==)

We denote it by

![]() :

and we call it autocorrelation at lag

:

and we call it autocorrelation at lag

![]() (the distance

(the distance

![]() between two terms of the sequence is called lag).

between two terms of the sequence is called lag).

When we observe the first

![]() realizations of a sequence

realizations of a sequence

![]() ,

we can compute the sample autocorrelation at lag

,

we can compute the sample autocorrelation at lag

![]() :

:![[eq11]](/images/autocorrelation__21.png) where

where

![]() is the sample

mean

is the sample

mean

If

![]() is covariance stationary, then the numerator of

is covariance stationary, then the numerator of

![]() is a consistent estimator of

is a consistent estimator of

![]() and the denominator is a consistent estimator of

and the denominator is a consistent estimator of

![]() .

As a consequence,

.

As a consequence,

![]() is a consistent estimator of the autocorrelation at lag

is a consistent estimator of the autocorrelation at lag

![]() .

.

The autocorrelation function (ACF) is the function that maps lags to

autocorrelations, that is,

![]() is considered as a function of

is considered as a function of

![]() (see the examples below).

(see the examples below).

When the mapping is from lags to sample autocorrelations

![]() ,

then we call it sample ACF.

,

then we call it sample ACF.

An ACF plot is a bar chart (or a line chart) that plots the autocorrelation function:

lags are on the x-axis;

the autocorrelations corresponding to the lags are on the y-axis.

Let's look at some examples of ACF and ACF plots.

Suppose that

![]() is a covariance stationary sequence such

that

is a covariance stationary sequence such

that![]() where

where

![]() is a constant and

is a constant and

![]() is an IID sequence of

standard normal

random variables (zero mean and unit variance).

is an IID sequence of

standard normal

random variables (zero mean and unit variance).

Such a sequence is called an autoregressive process of order 1, or AR(1) process (the order is the maximum lag of the sequence on the right hand side of the equation).

Note that

![[eq22]](/images/autocorrelation__37.png) where

we have performed recursive substitutions of

where

we have performed recursive substitutions of

![]() with

with

![]() .

.

By using this expression for

![]() ,

we can easily derive the autocovariance at lag

,

we can easily derive the autocovariance at lag

![]() :

:![[eq24]](/images/autocorrelation__42.png) where:

in steps

where:

in steps

![]() and

and

![]() we have used the

bilinearity of the

covariance operator and in step

we have used the

bilinearity of the

covariance operator and in step

![]() we have used the facts that 1) the covariance of a random variable with itself

is equal to its variance; 2) the covariance between

we have used the facts that 1) the covariance of a random variable with itself

is equal to its variance; 2) the covariance between

![]() and

and

![]() is zero for any

is zero for any

![]() because

because

![]() depends only on

depends only on

![]() for

for

![]() and the sequence

and the sequence

![]() is IID.

is IID.

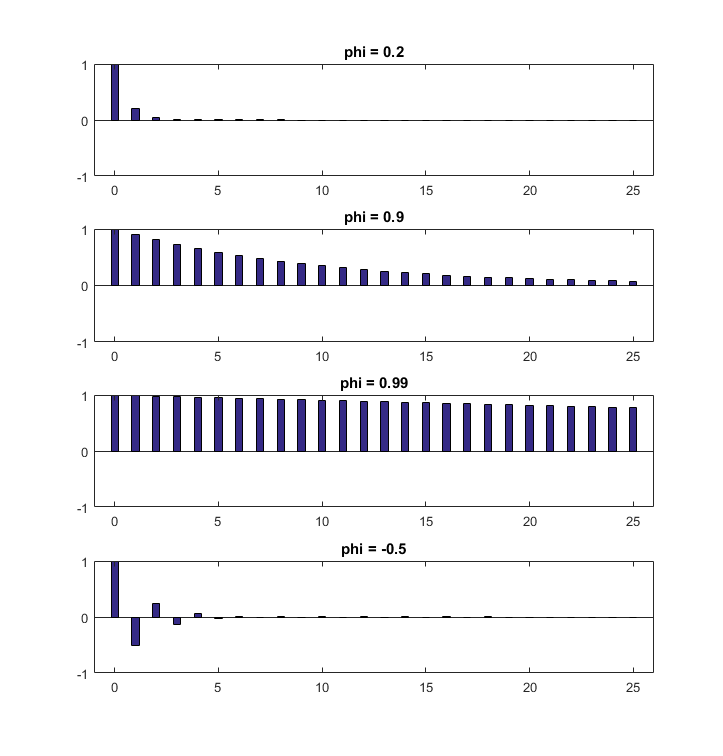

Thus, the autocorrelation at lag

![]() is

is![[eq26]](/images/autocorrelation__54.png)

The following ACF plots show the autocorrelation function for different values

of

![]() .

.

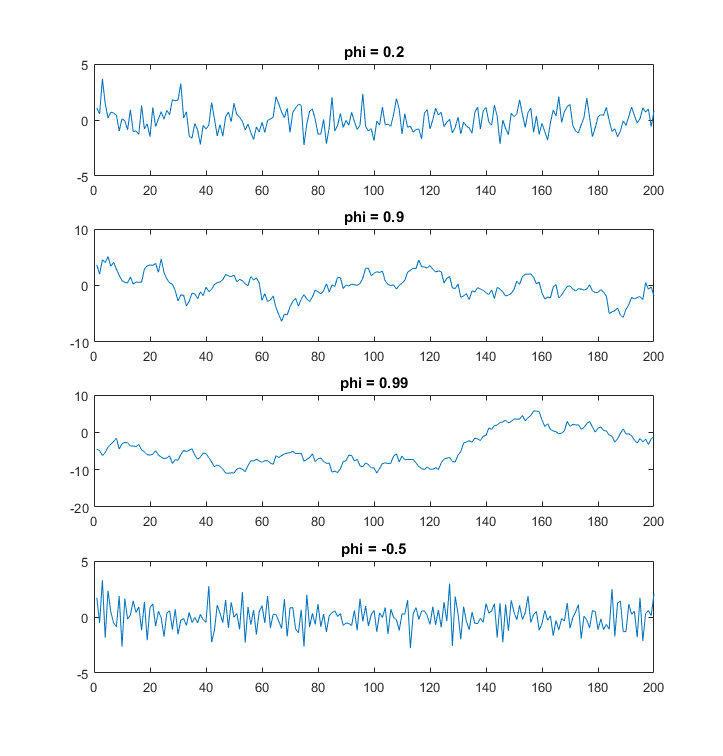

In this example, we show what a sample ACF looks like.

We generate, via Monte Carlo simulations, 200 realizations for each of the four AR(1) processes whose ACFs have been plotted above. The realizations are plotted below.

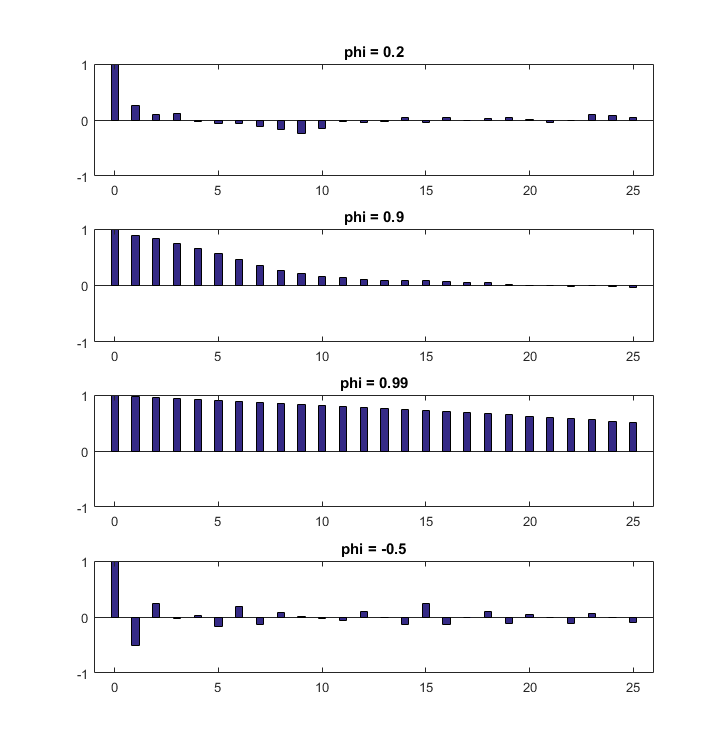

We then compute their sample ACFs, which are plotted below.

These are the sample versions of the ACFs shown in Example 1. As the sample autocorrelations are noisy estimates of the true autocorrelations, these ACFs do not coincide with those shown in Example 1.

Please cite as:

Taboga, Marco (2021). "Autocorrelation", Lectures on probability theory and mathematical statistics. Kindle Direct Publishing. Online appendix. https://www.statlect.com/fundamentals-of-statistics/autocorrelation.

Most of the learning materials found on this website are now available in a traditional textbook format.